Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The right home is out there, you just have to find it. This may seem like an oversimplification of the home search process, especially for first-time home buyers who haven’t been through it before. But once you’ve figured out your budget and discussed your needs with your real estate agent, you’ll be off and running. Here is a quick guide to help you get started on your home buying journey.

How to Search for a Home

Which houses can I afford?

Before you go perusing pages and pages of listings online, you’ll want to know your budget. Remember that while a home’s listing price is the main character in the list of home buying expenses, it’s not the only cost you’ll encounter. Knowing the full spectrum of the costs associated with buying a home will help you paint a clear picture of what you can afford. Once you’re familiar with these costs, you can strategize ways to save money to buy a house and plan to make a down payment.

To get an idea of what’s affordable, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different down payment amounts to get estimates of your monthly payment for any listing price.

Mortgage Pre-Approval

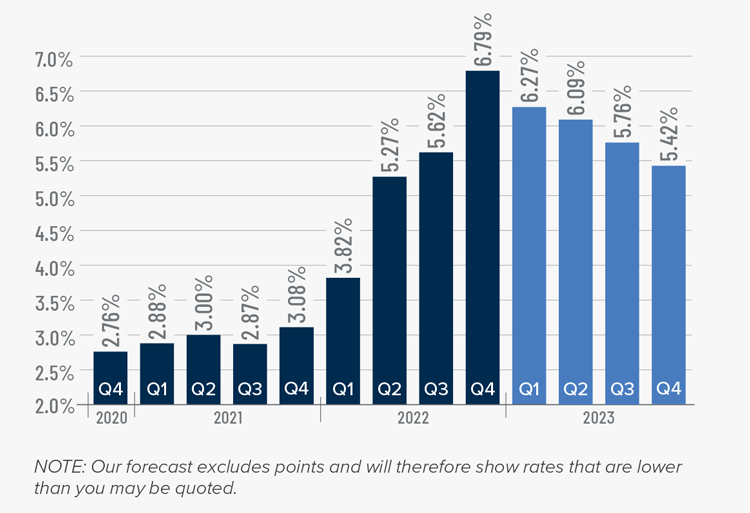

Another way you can supercharge your home search efforts is to get pre-approved for a mortgage. Pre-approval has several benefits for prospective home buyers. It helps you understand the different types of home loans available to you and what interest rate you can expect when the time comes to lock in your mortgage. It also streamlines the home buying process once you’ve found the property you’d like to pursue.

Image Source: Getty Images – Image Credit: Georgijevic

How do I find the right home?

Understanding your needs as a homeowner will help you narrow your selection pool. Before you start your home search, make a list of must-have and nice-to-have home features. This will inform your discussions with your real estate agent. Once they know what you consider a dealbreaker, they can pinpoint the right candidate homes.

So, where can you find available homes? Yes, driving around your neighborhood looking for “For Sale” signs is one way to go about it, but a vast majority of home shopping occurs online. Real estate websites like Windermere.com have advanced home search tools that allow you to filter by location, price, number of bedrooms and bathrooms, etc., plus helpful features like virtual tours, professional photography, maps, and more.

What are the different house styles?

Familiarizing yourself with the different architectural styles will help to inform your home search. Understanding the differences between a Craftsman home and a Cottage home can make a big difference when you’re house hunting. Each style has its own unique characteristics, perspective on space, and flair. Knowing what kind of architecture and home design you’re drawn to will also help your agent conduct more efficient home searches.

Working with a Real Estate Agent

Your real estate agent will be your greatest resource during your home search. They have access to the Multiple Listing Service (MLS), the largest network of homes on the market. Your agent will use the MLS to create customized searches for available listings and can easily connect with sellers’ agents to coordinate next steps.